Canada explores the Digital Dollar

Canada explores the Digital Dollar

Americans increasingly fearful about banks, Revolut turns on UK

The New Money Brief covers the global rise of digital currencies and how they are disrupting the world of payments, and much else.

Delivered several times a week. Created and edited by Marc Andrew.

The Bank of Canada (BoC) on Monday launched public consultations on the features that could be included in a digital Canadian dollar (CBDC), in an exploratory move to gauge the viability of a digital version of the currency.

Central banks across the world are studying digital versions of their currencies to avoid leaving digital payments to the private sector as the decline of cash has accelerated in some cases due to the COVID-19 pandemic.

China has been a leader among countries that are developing central bank digital currencies (CBDC), although adoption is still in the early stages. The central banks of Japan, Brazil and Australia have also taken steps toward launching a digital token.

Policymakers said they will take submissions until June 19.

Source: Reuters

Almost no one in the general public understands the concept of a CBDC and what it makes it different from the digital money they already use every day.

The Bank of Canada’s own explanation is here. McKinsey tries here.

The most important differences between CBDCs and today’s digital money are:

Issuing authority: CBDCs are issued and backed by a country's central bank, while the digital money in your bank account is a liability of your commercial bank. This means that CBDCs carry the full faith and credit of the central bank, while the digital money in your bank account is only as secure as the commercial bank it is held with.

Underlying technology: CBDCs may be based on distributed ledger technology (DLT), such as blockchain, which allows for a decentralized and more transparent system. In contrast, the digital money in your bank account is part of a centralized ledger system managed by your bank and is dependent on the bank's internal systems and databases.

Nature of the currency: CBDCs are considered a digital form of fiat currency, having the same legal tender status as physical banknotes and coins. This means that - potentially - they can be used for payments and settlements without the need for a third party, like a commercial bank.

Privacy and anonymity: CBDCs - in their retail version at leasy - open up the potential for all transactions to be tracked on the central banks own databases. For many, this is an Orwellian prospect. Banks argue they would design the currency with plentiful privacy.

On this last point: there are two versions of a CBDC: wholesale and retail.

Wholesale transactions happen among major banks and central banks, and will almost certainly see full digitisation on a ledger within months or years.

Retail CBDC’s, in which the central bank begins to interact with citizens on an everyday level directly, are still a ways away and much more open to question. These are open to major concerns of privacy and control, not to mention systemic uncertainty, as the head of the IMF said last week. They’re currently being actively tested in China and a few other countries.

In short, CBDC’s are central banks’ answer to bitcoin (and crypto), in the event the latter maintains the rise in influence it’s seen in its first decade.

If you’re interested in the global race toward CBDC’s. the Atlantic Council keeps a good resource here: www.atlanticcouncil.org/cbdctracker.

On with the Brief!

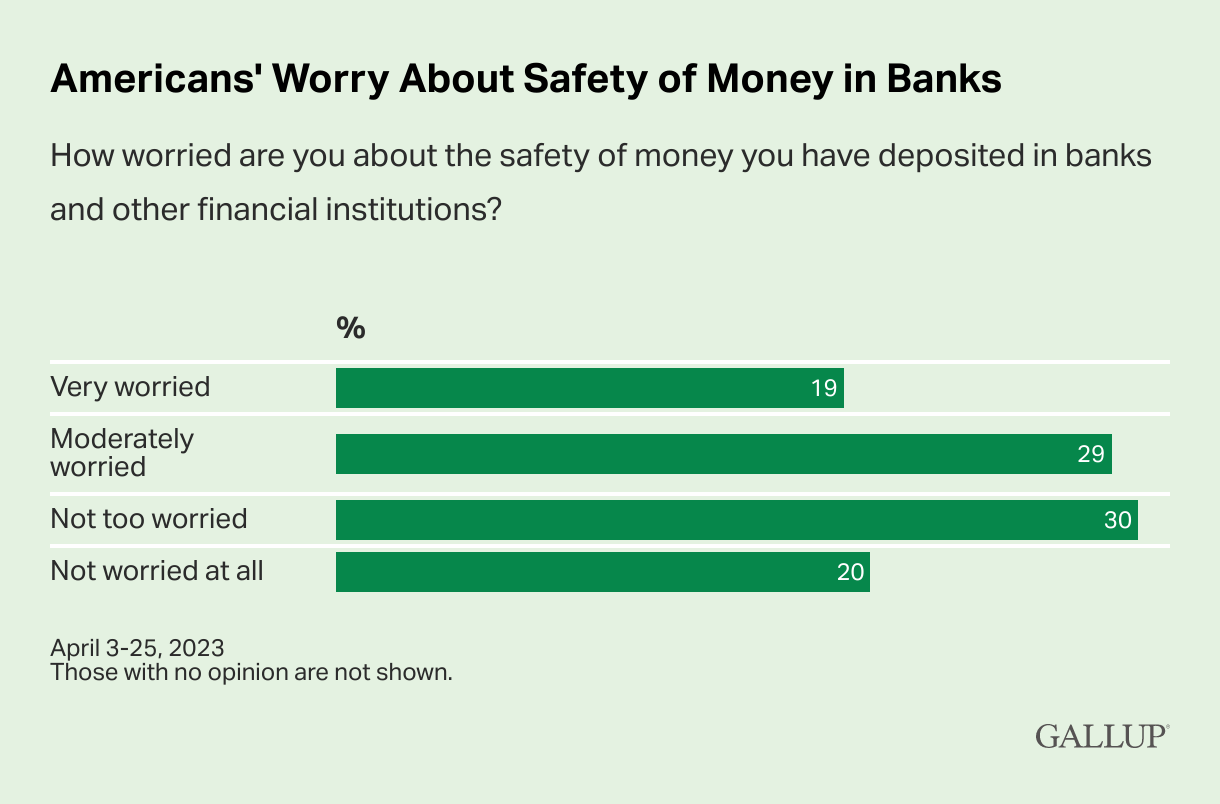

Amid turbulence in the U.S. banking system, nearly half of Americans are anxious about the safety of the money they have in accounts at banks or other financial institutions. A total of 48% of U.S. adults say they are concerned about their money, including 19% who are “very” and 29% who are “moderately” worried. At the same time, 30% are “not too worried” and 20% are “not worried at all.”

The latest readings are similar to those in 2008. In September of that year, shortly after the collapse of Lehman Brothers, which remains the largest bankruptcy filing in U.S. history, 45% of U.S. adults said they were very or moderately worried about the safety of their money.

Several months later, in December, after Congress’ Troubled Assets Relief Program (TARP) bailed out other banks in danger of failing, Americans were slightly less concerned about the safety of their personal financial accounts, as 41% said they were very or moderately worried.

Source: GALLUP

More than a million investors around the world were left stranded when FTX suddenly collapsed in November with an astonishing hole, estimated at $8.7 billion, in its balance sheet. The cryptocurrency exchange and its 130-plus affiliates have been operating in bankruptcy for five months, and a new management team claims to have recovered $7.3 billion of the missing cash and tokens. Yet only one component of the company has returned money to clients: FTX Japan.

FTX’s Japanese unit allowed all verified accounts to resume withdrawals on February 21. As of April 25, nearly 10,000 individual and corporate clients had withdrawn crypto and cash worth approximately 23.4 billion yen ($175.4 million), according to the company.

Count this as a victory for Japan’s financial regulators and the strict rules they’ve put in place to protect consumers in the wild and wooly world of crypto.

Japan cracked down with safety and soundness rules from a unified regulator after two big exchange hacks. But now, from that stable (and some in the industry would say overly restrictive) base, it’s seeking to come up with a strategy to become a leader in the collection of mostly decentralized, blockchain-based technologies known as web 3.

The U.S., by contrast, has arguably been open to more innovation, but its dueling oversight agencies and lack of rules have created gaps in oversight and a culture of regulation by enforcement that makes strategic planning perilous.

Source: Forbes

Liechtenstein Prime Minister Wants Citizens to Pay for Government Services With Bitcoin

Although details of the plan were sparse, in a recent interview Prime Minister Daniel Risch said that a “Bitcoin payment option is coming.”

He went on to describe how the European microstate intends to accept payment for government services in Bitcoin. It will then immediately exchange them for Swiss francs, the national currency.

A similar approach to Bitcoin payments has been used by the Swiss communities Zug and Lugano. There, local authorities have moved to make Bitcoin payments legal for the payment of certain taxes and public service expenses. In Lugano, even McDonalds accepts Bitcoin.

Moreover, the latest news is not the first time Liechtenstein has made headlines

Source: BeInCrypto

The co-founders of Revolut, one of the darlings of the UK technology scene, have strongly criticised Britain as a place to run a business, complaining of high taxes, red tape and a skills shortage, adding that they would never consider a flotation on the London Stock Exchange.

Nik Storonsky, the chief executive, and Vlad Yatsenko, chief technology officer, said that although there was a lot of talk by the government about promoting Britain as a science and technology superpower, there was “very little action” especially compared with the United States.

Source: The Times UK

Wyoming Adopts Stable Token Legislation and Lays the Foundation for a Government-Issued Stablecoin

Wyoming’s recently enacted Stable Token Act is the latest step in the Cowboy State’s efforts to create a business and legal environment that is tailored to digital assets and blockchain businesses. It also cements Wyoming’s position in the debate among regulators and the private sector around the types of entities that can – or should – issue stablecoins.

The Act creates a path for Wyoming to issue the United States’ first government-issued stablecoin, which would be fully backed by reserves of US dollars. However, the law is short on specifics and the committee created by the Act to develop the Wyoming stablecoin will have a list of open issues and challenges to overcome before the first token issuance.

In addition, legal and practical uncertainties exist around Wyoming’s ability to issue a stablecoin, some of which were highlighted in an open letter from Wyoming’s governor announcing that he would allow the legislation to pass into law without his signature.

Source: Mayer Brown

BNP Paribas is partnering with Bank of China (BOC) to promote China’s digital fiat money to its corporate clients, the French bank said in a statement on Thursday.

The collaboration allows BNP Paribas China to connect with BOC’s system and launch an e-CNY management system for its corporate clients. China has so far authorised 10 banks, all domestic lenders, to handle its digital currency business.

The system can “link [the client’s] digital yuan wallet to its bank account” to facilitate “efficient, real-time and convenient [digital cash] practice”, BNP said in the statement.

In addition, the French bank will explore expanding usage of China’s central bank digital currency (CBDC), to smart contracts, supply chain finance, and for utility and cross-border payments, it said.

Source: South China Morning Post

China is putting the yuan front and center in its fight back against the US's unique influence over global money. President Xi Jinping's government has been busy striking deals over the past year to expand the ways in which the currency is used, with new agreements linked to the renminbi stretching from Russia and Saudi Arabia to Brazil and even France.

While the US remains the world’s clear financial hegemon, these moves are helping China to carve out a bigger place for itself in the international financial system. They come at a time when geopolitical strains are growing and global commerce is becoming an ever-more-active battleground.

Source: Yahoo! Finance

Singapore has taken another step forward in being a regional leader in trade digitisation as they continue to develop programmes and initiatives to support this transition. The Infocomm Media Development Authority (IMDA) recently announced the completion of a live shipment to Thailand through Singapore’s TradeTrust framework, using an Electronic Transferable Record (ETR), the equivalent document to a Bill of Lading.

This trade marks the world’s first ETR cross-border trade, highlighting the industry’s progress towards a more digitalised future.

The trade was conducted using Singapore’s TradeTrust framework, which was pioneered by IMDA. TradeTrust comprises globally-accepted standards that connect governments and businesses to a public blockchain to enable the interoperability of electronic trade documents across digital platforms. It allows end users to digitally endorse, exchange and verify documents and effect title transfer.

Source: Trade Finance Global

It is still unclear what role blockchain will play in central bank digital currency development. However, even if CBDCs eschew blockchain technology when they are first minted, there is a growing ecosystem of digital assets and tokenised value operating on distributed ledgers and permissionless blockchains that central banks cannot ignore.

To better understand blockchain technology, Magyar Nemzeti Bank has developed an innovative programme which allows them to use and experiment with blockchain technology in a live field environment. Through non-fungible tokens, the MNB is issuing its own digital instrument on a private blockchain to exploit hands-on experience around the technology and set value parameters in the tokens themselves.